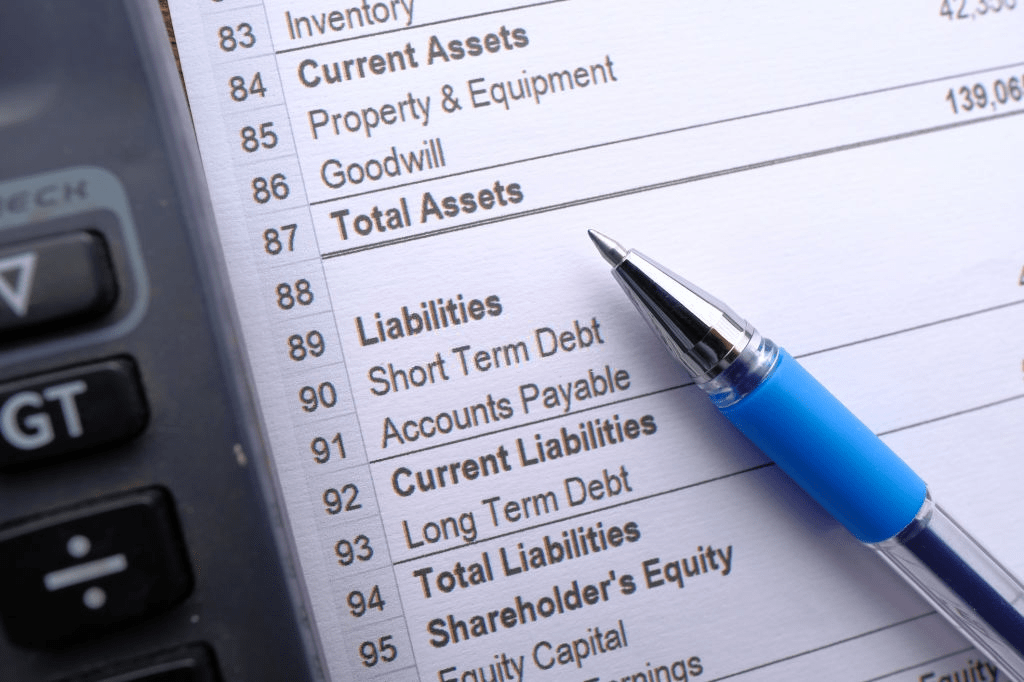

It is significant that advantages and liabilities are appropriately arranged on the Balance Sheet. To get a more clear image of the business, an administrator should separate the Balance Sheet into subcategories. The breakdown is clarified as follows:

• Current Assets: resources with the existence not exactly a year (for example money, Mastercard receivables, stock and prepaid costs).

• Fixed Assets: resources with an actual existence more prominent than a year that legitimately credits to delivering income (for example gear, PCs, furniture and leasehold enhancements).

• Other Assets: resources with an actual existence longer than a year that isn’t straightforwardly engaged with the generation of income (for example security stores, trademarks and fine art).

Liabilities require a comparative characterization and are separated as follows:

• Current Liabilities: obligations due inside one year (for example creditor liabilities, gathered costs, transient advances and even blessing declarations).

• Long-Term Liabilities: obligations due that reach out past one year (for example notes payable or long haul leases).

There is such a great amount of data to be picked up from the Balance Sheet. For instance, an eatery and hoteliers that have huge obligations may have significant income issues. Recognizing the present obligations from the long haul obligations on the Balance Sheet help decide the short and long haul money needs, just as the business potential achievement. Restaurateurs and hoteliers who assume huge obligations after opening could be messing themselves up. The eatery may show huge benefits dependent on the Income Statement, yet the café might not have cash since it is paying out the exceptional obligation (which is uncovered in a critical position Sheet).

Important Links to discuss your business services:

CPA Firm New Jersey

CPA Firm Long Island

Accounting Firm New Jersey

Tax preparation services NJ